Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Cash App, the peer-to-peer fintech app owned by Jack Dorsey’s Block, has launched a new timed payment system that allows eligible users to pay for daily transfers over a longer period of time.

Companies have offered a large amount of money that is about to buy everyday products. About a year ago. DoorDash has partnered with Klarna – allowing users to “minimize” their purchases (this agreement inspired many jokes on the Internet “credit burrito” and late capitalism). The new Cash App is based on the current trend – increasing the flexibility of payments in P2P payments.

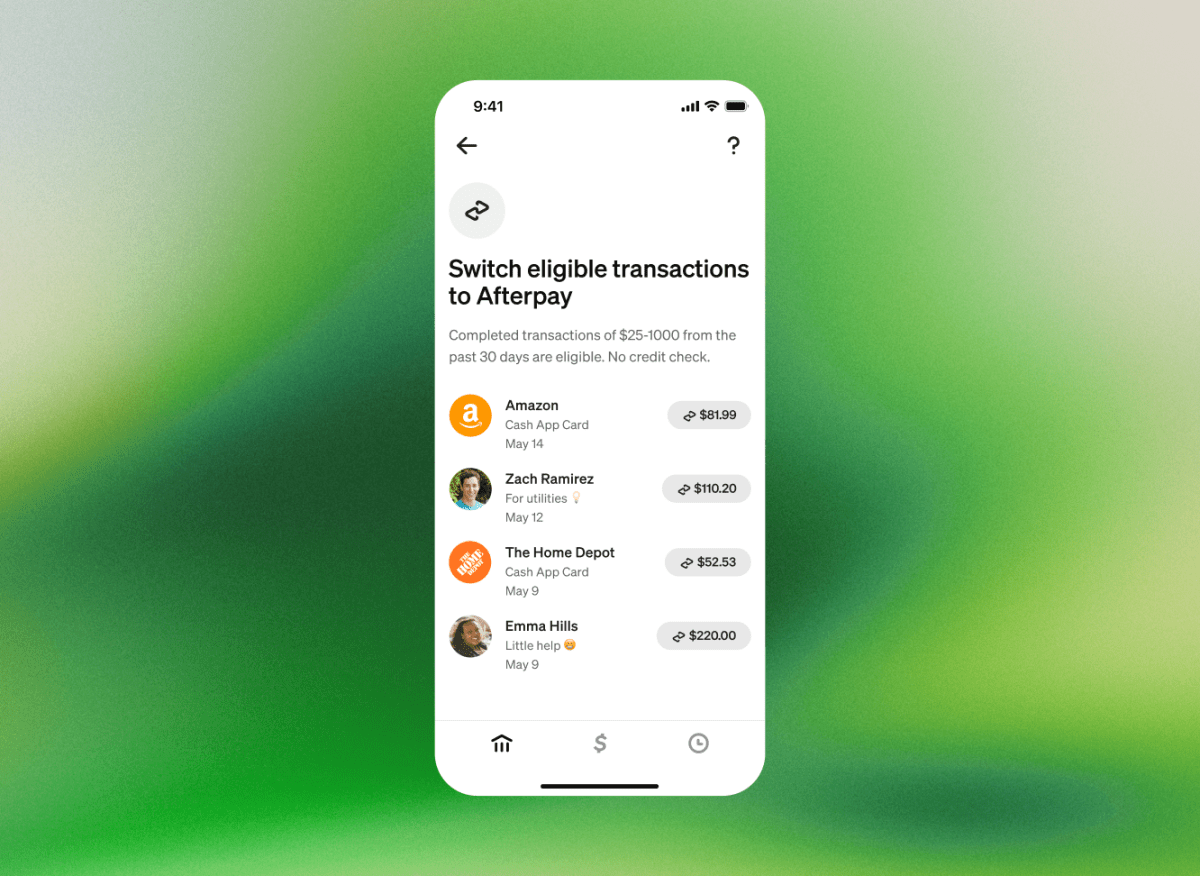

To use the new opportunity, users pay a 7.5% fee – which means that, if you borrow $ 100 from the Cash App, you will end up paying the company $ 107.50. Transfers of $25 or more are eligible, the company says, and withdrawals can be made in weekly increments over a six-week period or as one payment at a time.

There are still credit limits on new systems, but they are dynamic – meaning they will be different for different users. “The exact amount available for conversion depends on the number of transactions and customer reviews,” the spokesperson said. “We assess our performance for eligibility based on our lending criteria rather than traditional thresholds,” he added.

In an interview, Block’s Chief Executive Officer and Head of Business, Owen Jennings, framed the innovation as a way to add value to Cash App customers through “money management.” Jennings noted that most Americans have a variety of jobs today — many that pay more consistently than what was offered decades ago. The new Cash App is designed to increase financial flexibility for these transactions, Jennings said.

“We’re seeing a lot of people — especially young people — who are self-employed, entrepreneurs … (and) sports workers. They’re struggling, they’re working multiple jobs, (and) so they’re making different incomes,” Jennings said. “It’s very different if you go back 40 or 50 years ago – I think the highest income earners in the US (at that time) were getting, like, a regular W2 every two weeks.”

“Buy now, pay later” services have it it rose in popularity over the past few years it has also been causing a lot of criticism and concern. Some critics say that such services are designed to attract consumers credit lineswhile others have said that Americans who need money to buy household goods are a a sign of serious financial problems. Companies that offer this service have also found themselves in legal hot water. This week only, Klarna was charged on charges of “criminal activity”, reports Bloomberg.

Techcrunch event

San Francisco, CA

| |

October 13-15, 2026

Jennings said the new Cash App feature has built-in security features designed to keep users out of financial trouble, such as getting stuck in what he calls “debt”. “The way all of our rental products are designed is non-cyclical,” he added. If you do not repay the loan, then you will not be able to borrow another loan.

The service also builds on other money transfer services that Cash App already offers, Jennings said. In the last years, this program started Borrowingwhich, like a traditional bank, allows users to take out a small loan from the program and pay it back in four to six weeks.

Another offer is Afterpay for Cash App Card (its loan program), which allows users to delay payments made with the card.