Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Strong Crash: Amazon’s stock price has experienced a short-term correction in line with the broader market, but this trend is driven more by public sentiment than changes in the company’s fundamentals.

Quarterly Results Become a Turning Point: The third-quarter report was a powerful catalyst for the market to reassess Amazon’s trajectory. Not only did the company beat expectations on both major metrics, it did so convincingly: Earnings per share beat analysts’ expectations by 25%. The company’s shares rose more than 13% after the results were announced, reflecting investor optimism about earnings growth.

Growth drivers: Retail momentum strong, AWS accelerating

• AWS returns to dynamic growth: Its core cloud division’s year-over-year growth accelerated to 20%, an impressive figure for a company with approximately $130 billion in annual revenue. This signals new momentum and strengthens Amazon’s position in the race to be the AI leader.

• Retail segment shows operational efficiency: Contrary to previous expectations, the retail segment (North America and Global) started to contribute significantly to overall ROI. Its operating margins are growing, delivering long-awaited operating leverage. This is due to years of investments in automation and logistics, which now lower unit costs and expand gross margins.

Strategic advantages in the era of autonomy: Amazon structurally benefits from macro trends

1. Automation as a driver: Implementing autonomous systems reduces costs, allowing companies to simultaneously increase profit margins and lower prices for the end consumer. This creates a self-perpetuating cycle: volume growth, operating leverage, earnings per share growth, and additional investments in efficiency.

2. Vertical integration: Control of the supply chain from logistics centers to AWS cloud infrastructure creates unique and difficult-to-replicate entry barriers for competitors and ensures long-term cash flow stability.

Value Issue: Not cheap, but reasonable

Even though Amazon’s stock price is high, it doesn’t appear to be overvalued compared to its peers.

• The company trades at about 38 times forward earnings, trading at a deep discount to its five-year average.

• Compared to other companies on the Magnificent 7 list, Amazon is a reasonable value, especially compared to pricier companies like NVDA or TSLA.

• High capex on AI infrastructure ($116 billion over 12 months) puts temporary pressure on free cash flow. This is an investment in future growth, but investors should consider this factor.

Summarizing the quarter’s numbers and strategic metrics, Amazon’s positive outlook outweighs its risks (regulatory pressure, cyclical spending, and cloud competition).

Amazon combines maturity, operational efficiency, and acceleration with AWS and automation.

We believe Amazon is a top-ranked company in the M7 Index and will soon become one of the top companies in the Magnificent 7 Index.

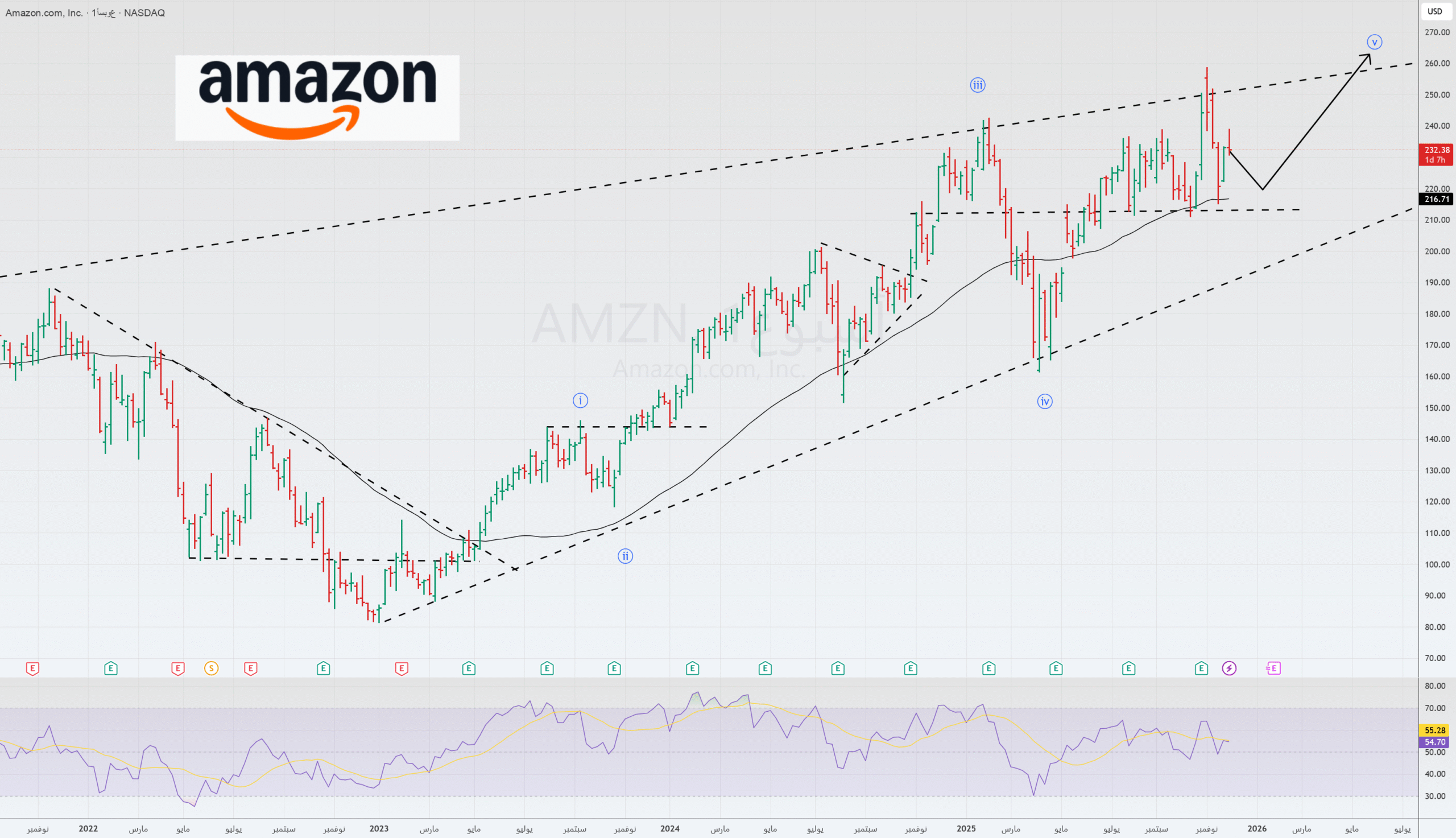

We see the fourth wave of correction coming to an end, with the stock reaching all-time highs soon.