Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

[ad_1]

With the U.S. 30-year Treasury yield returning to October 2023 levels and breaking through the 5% level, should we be concerned about systemic risks to the economy, country, and businesses? Will the Fed, led by Kevin Warsh, be forced to raise rates or at least hold rates longer?

It is important to consider the following data:

• U.S. 30-year bond yields return to 2007 levels

• US 10-year bond yields are approaching 5%.

• Variable rate corporate debt accounts for 40% of total U.S. corporate debt

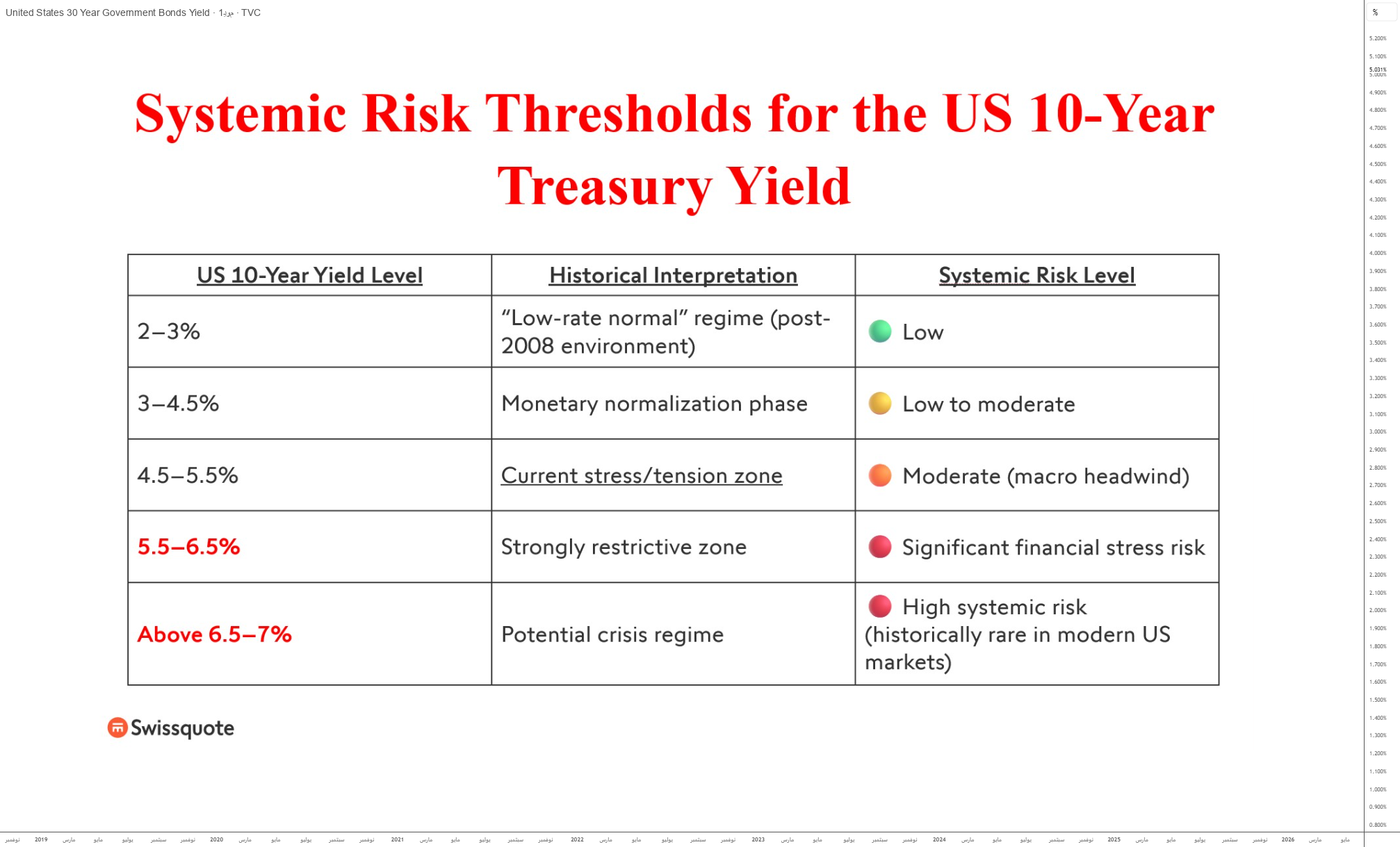

• But the systemic risk threshold has not yet been reached; somewhere between 6.5% and 7%.

In this context, it is necessary to distinguish between situations of high financial stress and true systemic risks. Historically, as long as nominal growth remains strong and financing flows continue to be normal, the U.S. bond market has been able to fluctuate between 4% and 5.5% on 10-year notes without triggering a global crisis. Current levels largely reflect the repricing of risks resulting from persistent inflation, geopolitical uncertainty and a deteriorating U.S. fiscal outlook.

The chart below shows the weekly Japanese candlestick for the U.S. 30-year bond yield, with financial risk areas identified by yield level.

The main channel of transmission to the economy is not immediate but gradual. U.S. companies rely primarily on the bond market for financing at fixed rates, which means rising interest rates are not immediately passed on to all debt. But with every new issuance or refinancing, the marginal cost of financing rises rapidly. However, the existence of about 40% of variable-rate debt has accelerated the transfer of interest effects in some industries, especially small businesses that rely on bank loans.

For the federal government, things have become more stringent compared to previous sessions. Higher long-term interest rates mechanically increase the cost of refinancing the public debt and increase the sensitivity of the federal budget to market conditions. This does not create default risk in the short term but reinforces the fragile dynamics of financial sustainability in the medium term.

So while the current area (near 5% in 10 years and over 5% in 30 years) represents significant levels of financial stress, the true threshold for systemic implosion is higher, around 6.5% to 7%, and the cumulative impact on sovereign debt, private credit and real estate could simultaneously become a major concern.

Disclaimer:

This content is intended for individuals familiar with financial markets and instruments and is for informational purposes only. The ideas presented (including market commentary, market data and observations) are not the work of any research department of Swissquote or its affiliates. This material is intended to highlight market trends and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is recommended that you seek professional advice from a licensed advisor before making any financial decisions.

The content is not intended to manipulate markets or encourage any specific financial behavior.

Swissquote makes no representations or warranties regarding the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The opinions expressed are those of the advisor and are for educational purposes only. Any product or market-related information provided should not be construed as advice on investment strategies or trading. Past performance is no guarantee of future results.

In no event shall Swissquote, its employees and representatives be liable for any damages or losses arising directly or indirectly from decisions based on this content.

The use of any trademark or third-party trademark is for reference only and does not imply endorsement by Swissquote Bank or that the trademark owner authorizes Swissquote Bank to promote its products or services.

Swissquote is a subsidiary of Swissquote Bank Ltd (Switzerland) regulated by the Swiss Securities Regulatory Authority (FINMA), Swissquote Capital Markets Limited regulated by the Cyprus Securities and Exchange Commission (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the Cyprus Financial Supervisory Authority, Swissquote Ltd (UK) regulated by the Cyprus Financial Supervisory Authority, Swissquote Financial Services (Malta) Limited Event Marketing Brands of the Malta Financial Services Authority, Swissquote MEA Ltd. (United Arab Emirates) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) regulated by the Hong Kong Securities and Futures Authority and Swissquote South Africa Limited (Pty) regulated by the Securities and Exchange Commission.

Swissquote products and services are available only to persons permitted to receive them by local law.

All investing involves some degree of risk. The risk of loss from trading or holding financial instruments can be substantial. The value of financial instruments (including, but not limited to, stocks, bonds, cryptocurrencies and other assets) may fluctuate up and down. There is a significant risk of financial loss when buying, selling, holding, betting or investing in these financial instruments. SQBE does not make any recommendation regarding any specific investment or transaction or the use of any specific investment strategy.

CFDs are complex instruments and carry a high risk of losing money quickly due to leverage. The vast majority of retail client accounts will suffer capital losses when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital assets are unregulated in most countries, and consumer protection rules may not apply to them. As a speculative investment with high volatility, digital assets are not suitable for investors who cannot bear high risks. Make sure you understand each digital asset before trading.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainty.

The use of Internet-based systems may involve high risks, including but not limited to fraud, cyberattacks, network and communications failures, and identity theft and phishing attacks related to digital assets.

[ad_2]

Source link