Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

[ad_1]

oneFirst of all, the reasons for such a serious imbalance in the RMB exchange rate are as follows:

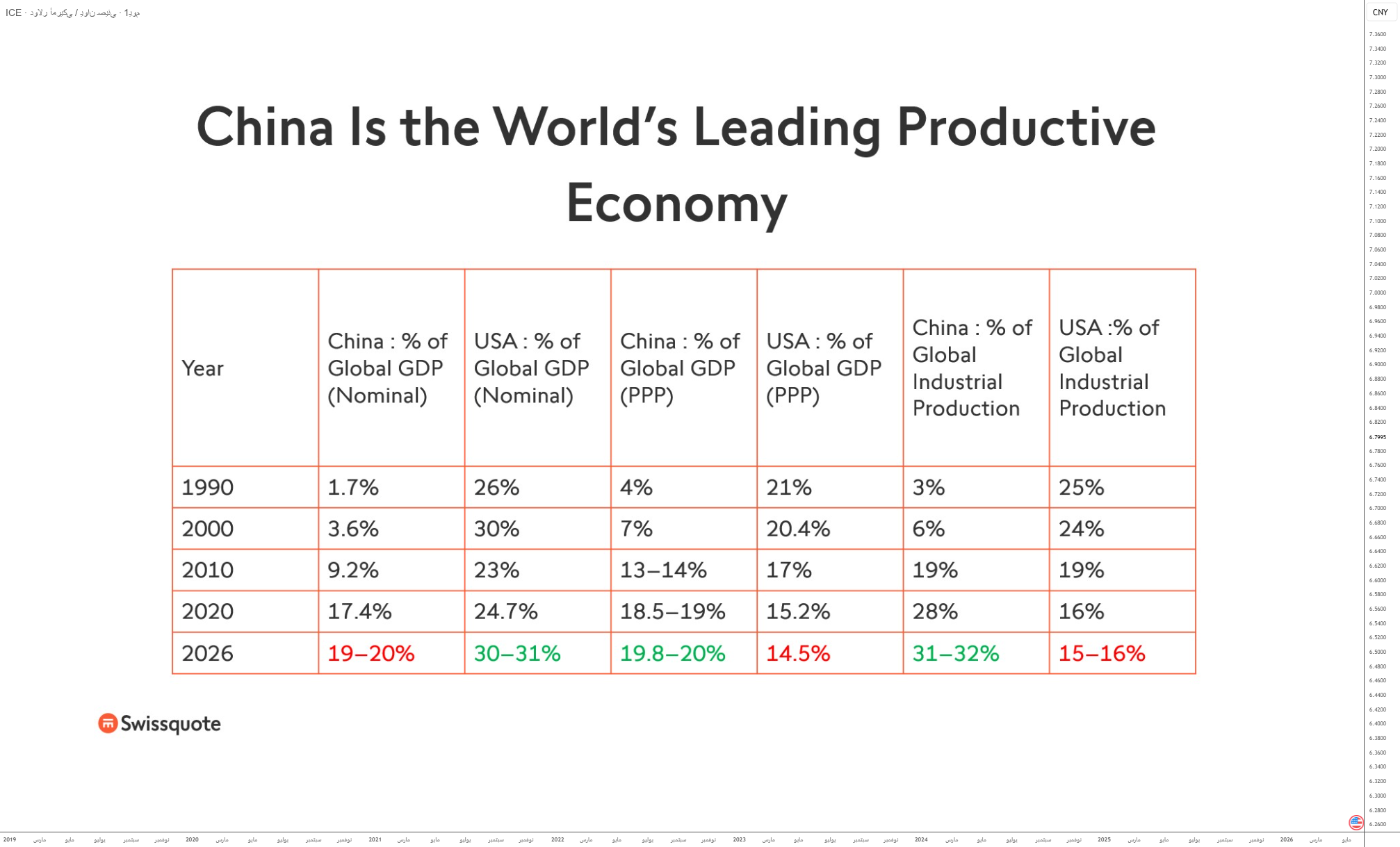

• Today, based on PPP-adjusted GDP, China has become the world’s largest productive economy, while the United States has fallen to second place.

• However, the United States still ranks first in terms of nominal GDP. The truth lies between nominal output and purchasing power-adjusted output, so it can be considered that China and the United States are tied for first in the world today.

• In terms of pure industrial production, China is considered the world’s factory, accounting for 32% of global industrial production, while the United States only accounts for 16%.

• Herein lies the imbalance: Although China’s economic power is similar to that of the United States, China still ranks only fifth, far behind the United States as a global monetary and financial power.

The table below shows the position of the United States and China in the global economy based on a number of criteria, including nominal gross domestic product, output adjusted for purchasing power parity, and global industrial production.

In the long run, this imbalance will gradually narrow, and in a few decades the Chinese yuan (CNY) will gradually catch up with the US dollar. However, it will take a long time for the RMB to finally become equivalent to the US dollar in the global monetary system. The most important thing is that it requires a series of basic structural factors.

The first factor is the gradual opening up of China’s financial system. Even today, the yuan is not considered a fully convertible currency and capital flows are still largely controlled by Beijing. While any dominant global currency would need to be freely traded internationally. As long as foreign investors do not have complete free access to the Chinese market, the yuan’s global expansion will be limited.

The following data reveals the five largest global currencies within the global financial and monetary system based on several key criteria. In terms of market share in the foreign exchange market, the RMB ranks only fifth.

The second major factor will be the development of a massive Chinese bond market capable of competing with U.S. Treasuries. The U.S. dollar dominates primarily because the U.S. provides the world with the ultimate financial safe haven: U.S. Treasuries. For the yuan to continue to appreciate, China must build a deep, highly liquid bond market that is trusted by central banks around the world.

The third factor is the yuan pricing of commodities, especially oil. Even today, the vast majority of global oil trade is conducted in U.S. dollars. If more and more Russian, Gulf or African energy exports are settled in RMB in the future, this will automatically increase the global structural demand for RMB.

The fourth factor is the rise of China’s geopolitics and the gradual formation of an Asian economic bloc centered on Beijing. The more trade flows between Asia, the Middle East, Africa and BRICS countries, the greater the international role of the RMB.

Finally, the most important factor is trust. Global currencies depend not only on economic strength but also on the political, legal and financial stability of the issuing country. The U.S. dollar still enjoys a huge historical advantage in this area.

Therefore, the yuan may become equivalent to the US dollar within the next 20 years, but only if all these structural factors align at the same time.

Disclaimer:

This content is intended for individuals familiar with financial markets and instruments and is for informational purposes only. The ideas presented (including market commentary, market data and observations) are not the work of any research department of Swissquote or its affiliates. This material is intended to highlight market trends and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is recommended that you seek professional advice from a licensed advisor before making any financial decisions.

The content is not intended to manipulate markets or encourage any specific financial behavior.

Swissquote makes no representations or warranties regarding the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The opinions expressed are those of the advisor and are for educational purposes only. Any product or market-related information provided should not be construed as advice on investment strategies or trading. Past performance is no guarantee of future results.

In no event shall Swissquote, its employees and representatives be liable for any damages or losses arising directly or indirectly from decisions based on this content.

The use of any trademark or third-party trademark is for reference only and does not imply endorsement by Swissquote Bank or that the trademark owner authorizes Swissquote Bank to promote its products or services.

Swissquote is a subsidiary of Swissquote Bank Ltd (Switzerland) regulated by the Swiss Securities Regulatory Authority (FINMA), Swissquote Capital Markets Limited regulated by the Cyprus Securities and Exchange Commission (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the Cyprus Financial Supervisory Authority, Swissquote Ltd (UK) regulated by the Cyprus Financial Supervisory Authority, Swissquote Financial Services (Malta) Limited Event Marketing Brands of the Malta Financial Services Authority, Swissquote MEA Ltd. (United Arab Emirates) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) regulated by the Hong Kong Securities and Futures Authority and Swissquote South Africa Limited (Pty) regulated by the Securities and Exchange Commission.

Swissquote products and services are available only to persons permitted to receive them by local law.

All investing involves some degree of risk. The risk of loss from trading or holding financial instruments can be substantial. The value of financial instruments (including, but not limited to, stocks, bonds, cryptocurrencies and other assets) may fluctuate up and down. There is a significant risk of financial loss when buying, selling, holding, betting or investing in these financial instruments. SQBE does not make any recommendation regarding any specific investment or transaction or the use of any specific investment strategy.

CFDs are complex instruments and carry a high risk of losing money quickly due to leverage. The vast majority of retail client accounts will suffer capital losses when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital assets are unregulated in most countries, and consumer protection rules may not apply to them. As a speculative investment with high volatility, digital assets are not suitable for investors who cannot bear high risks. Make sure you understand each digital asset before trading.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainty.

The use of Internet-based systems may involve high risks, including but not limited to fraud, cyberattacks, network and communications failures, and identity theft and phishing attacks related to digital assets.

[ad_2]

Source link