Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

[ad_1]

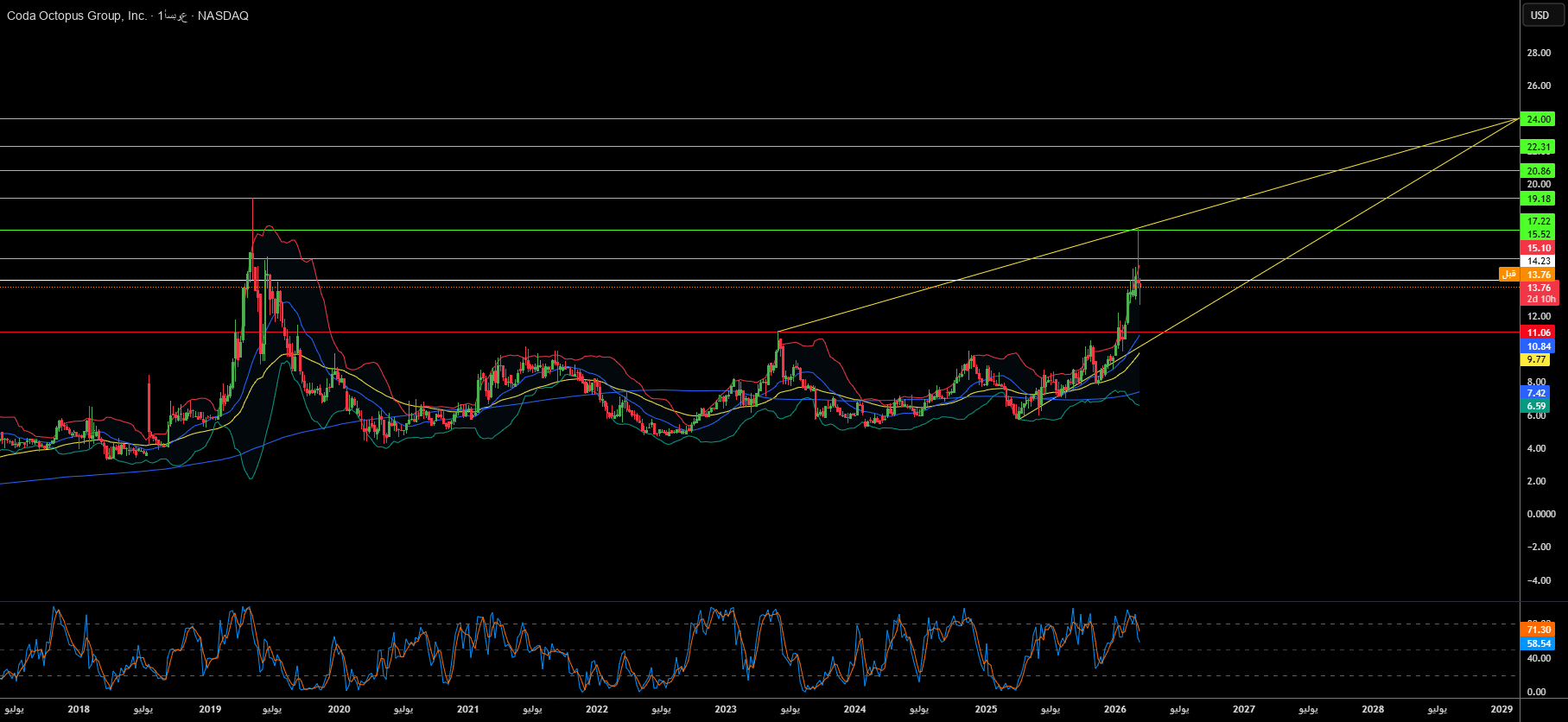

CODA Group holds an incredibly dominant position for a company of its size in the rapidly escalating underwater theater of war. Total revenue in fiscal year 2025 was US$26.56 million, a year-on-year increase of 30.7%. Earnings before interest, taxes, depreciation, and amortization (EBITDA) surged 71.3% to US$7.61 million, with a gross profit margin of 68.91%. These numbers are not specific to a startup struggling to find its footing. Rather, it is the financial footprint of a technology monopoly operating in a market that is structurally forced to grow. Driven by competition for Arctic resources and rising maritime tensions in the Asia-Pacific region, the value of the global undersea warfare sector will reach $15.69 billion in 2025 and is expected to double to $28.78 billion by 2034.

At the heart of Coda Octopus’s competitive moat is its proprietary Echoscopy PIPE architecture, a real-time volumetric sonar system that processes a staggering 81 million data points per acoustic pulse. While traditional sonar systems generate planar 2D images that require hours of post-processing, PIPE provides real-time 5- and 6-dimensional visualization of backscatter with an angular resolution of less than 0.3 degrees, even in conditions of zero visibility and extreme turbidity. This set of patents covers radial data compression, audio object representation, and augmented reality data fusion, completely preventing competitors from adopting this approach in hardware. This technology exclusivity enables Koda Octopus to achieve sole supplier status with Raytheon and Northrop Grumman on mission-critical programs, generating high-margin recurring revenue streams that define the economics of defense platforms.

The company’s Augmented Diver Display (DAVD) also expands its strategic footprint in special operations. Officially designated for use by the U.S. Navy, the DAVD system transforms a standard diving helmet into a real-time heads-up display, reducing mission times in zero-visibility conditions from hours to minutes. U.S. Special Operations Command has ordered 16 radio units through 2025 to increase the program’s operational credibility. With a debt-free balance sheet, $30.4 million in liquid cash, and only 11.27 million shares of limited equity, management maintains ample flexibility to acquire growth while preventing stock dilution, a rare shareholder-friendly discipline among small defense companies.

The geopolitical context reinforces all structural drivers. China’s formal establishment of dual-use principles in the Arctic by 2025, 14 container voyages through Arctic shipping lanes, and increasing maritime investments in Japan and India all underscore the urgency behind Koda Octopus’ technology. Key risks remain revenue concentration from defense contracts, volatility in small-cap companies, and employee retention challenges, but CODA presents a coherent and compelling argument for investors looking for real technology differentiation in a market with strong demand growth. The invisible battlefield is real, it’s growing, and Coda Octopus may be the only company that can clearly see it.

[ad_2]

Source link